BLOGS

BLOGS  NEWSROOM

NEWSROOM  CASE STUDIES

CASE STUDIES  WEBINARS

WEBINARS  PODCASTS

PODCASTS  ASSET HUB

ASSET HUB  EVENT CALENDAR

EVENT CALENDAR

It is appalling to notice the difference a year can make! The coronavirus pandemic and the emerging economic fallout have drastically changed customers’ and workers’ needs, habits, and aspirations. The pandemic compelled the various industries of the economy to virtualize their operations; the insurance sector is no exception.

Different industrial sectors adapted to this shift quickly; insurers still face persistent obstacles to finding growth and profitability prospects. Regardless, this experience has paved the way to focus our efforts on innovation and investment in a digital future.

InsurTech plays a crucial role in integrating digital innovation with the insurance sector. Insurance technology trends modernize the traditional process of the insurance industry. These technologies enhance the efficiency and effectiveness of the operations of insurance companies.

Technology Trends in the Insurance Industry

New technologies will mold and shape the insurance industry. The Insurance technology trends will streamline various processes and smoothen up the road to developing various products catering to the current times and users.

Some insurance technology trends that can alter and transform the insurance industry are briefly discussed below.

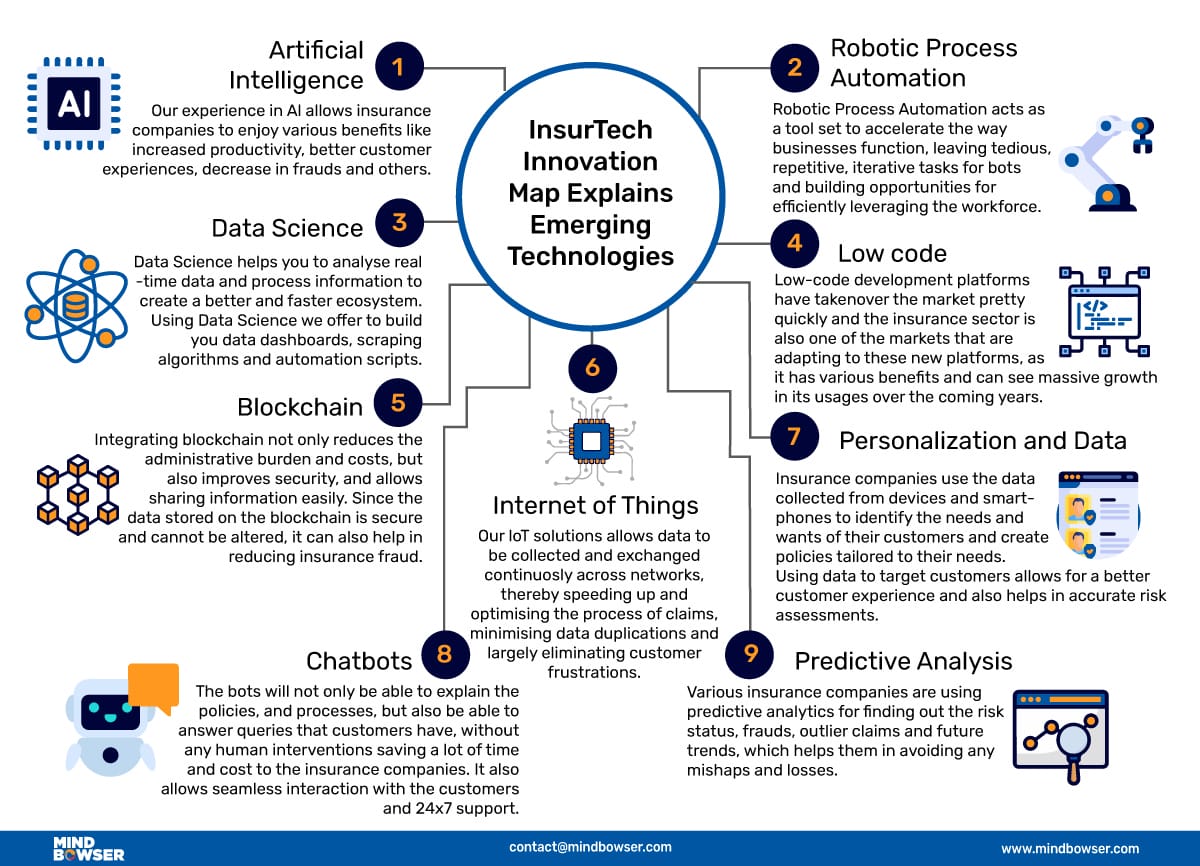

Fig: Emerging Insurance Technology Trends

Artificial Intelligence

The adoption of Artificial Intelligence is gaining momentum across industries. With AI, insurance companies can enjoy various benefits like increased productivity, better customer experiences, and decreased fraud.

With chatbots powered by AI, you can answer your customers’ queries around the clock; from solving simple policy-related issues to addressing concerns and grievances, you can do it all.

Insurance companies can examine historical data through machine learning and AI and recognize a collection of models that can be used to identify fraud at an early stage and prevent it from occurring.

Artificial Intelligence in the insurance industry allows Insurers to streamline the end-to-end process with AI. From data collection, the formation of settlements, authorization, and acceptance to monitoring payment, tracking of salvage and recovery, and processing of legal matters to contact management.

These AI-powered bots will review the claim, verify policy information, look out for fraud, and process payments, making the claims process quicker and more effective.

Digital consumers demand sophisticated products at affordable costs. With Artificial Intelligence, insurance agents gain comprehensive insights into the demographics, preferences, purchasing habits, and other consumers’ data.

The agent will use this knowledge and information to involve clients in their background and pitch policies per their needs, allowing the insurance organizations to tap the opportunity.

Digital Transformation in the Insurance Industry

Data Science

Data Science in the insurance industry helps insurers to develop successful strategies for acquiring new clients, developing tailored products, assessing risks, assisting underwriters, implementing fraud detection systems, and much more. Data scientists can easily segment an insurance agency’s customers through financial assets, age, location, or other demographics.

After finding similarities in their behaviors, interests, actions, or personal details, classifying clients into various categories helps insurance providers create desirable and useful plans for each category. This results in targeted cross-selling capabilities and customized goods being introduced that can be successfully promoted.

We have already discovered that data science will help insurers create tailored solutions that are more attractive to clients. This recommendation engine algorithm will recognize the tastes and peculiarities in customers’ choices from their account behavior and suggest customized items immediately to improve upselling and cross-selling revenue.

Risk evaluation will greatly minimize insurance losses. One area where risk management solutions can be applied to reduce risks is insurance underwriting. The underwriter’s ability to recognize the risks involved in insuring a customer or an asset will directly affect the company.

Data science allows AI and cognitive analytics to evaluate a client’s policy documents and determine the appropriate premium quantity and coverage amount recommended for that policy. It would significantly increase the performance of underwriters, making it easier to process low-risk guidelines rapidly.

We’ve implemented a solution for an insurance platform that involves seamless document scanning and parsing.

We’ve made the insurance platform better by creating a solution that makes scanning and understanding documents seamless. This improvement ensures a smoother experience for users dealing with insurance paperwork, allowing them to access information quickly and efficiently.

We Developed Smart Mirror Solution With Personal Health and Daily Activity Tracker

We built one of the most advanced Smart Mirrors for tracking healthcare data and providing actionable insights to the user to improve their health. The platform along with its mobile apps tracks user data from 100+ sources and puts them in front of the user on their bathroom mirror.

Internet of Things (IoT)

Currently, the Internet of Things in the insurance industry is in the middle of a significant digital transformation. Customers expect results immediately in today’s digitally savvy, fast-paced business climate. This is why businesses of every scale and line, including the insurance chain, are trying to enhance customer support and loyalty using digital means.

IoT allows data to be collected and exchanged continuously across networks, thereby speeding up and optimizing the claims process, minimizing data duplications, and largely eliminating customer frustrations. Customers will no longer have to waste months wading through paperwork, and now they can collect protection from their devices and handle claims more effectively.

Additionally, via digital media, they will finally have the means to track their coverage and claims easily. The insurance business model is focused on the risk management capacity of the insurance broker. This is why data has often been at the core of the insurance industry; the way insurance risk and returns are modeled heavily on information drives decisions.

Usually, insurers have had to rely on historical experience, long-term modeling, and information provided by the insured parties to produce reasonable risk groups. The constantly available data stream provided by IoT devices can dramatically alter this. It will allow insurers to make risk assessments that are vastly more detailed and personalized.

The good risk will always subsidize the bad risk, and there is no real way around it. More and more precise risk models, however, would result in more equal premiums. Data from connected devices would also enable insurers to understand their clients at a deeper, better level due to more detailed and comprehensive data.

Industrial IoT (IIoT) Trends Report 2020

Cloud Computing

Another technology that has grown popular over the years is cloud computing. It is undeniable that cloud computing in the insurance industry can allow insurance companies to manage their costs very smoothly.

The insurance industry will potentially save a huge amount of money by introducing cloud-based technology that could be invested in several other important areas. Also, cloud adoption ensures versatility and performance and enhances business processes.

Unlike conventional IT services, cloud computing requires very limited implementation time. It enables companies to optimize their outstanding services and functionality quickly. In addition, cloud computing has enough tools at its disposal that are adequate for the numerous users in the shared world.

Not only are these resources efficiently, but they are also scalable. With their stable features and flexibility, cloud-based applications help insurance companies minimize overhead costs and streamline operations. The insurers could free up space in their budget seamlessly and help the workers concentrate on more important items.

AWS Vs Azure Vs GCP: Finding The Right Cloud Computing Service For You

Robotic Process Automation (RPA)

Robotic Process Automation in the insurance industry provides a non-invasive way to simplify key processes for insurance firms. In addition, automation offers a stable solution for an industry burdened with repetitive and mundane activities to maximize organizational effectiveness, customer loyalty, and profitability.

Large-volume claims forms can be carried out with just a third or half of the people needed compared to when the process was manual. This, in turn, has additional benefits because it provides immense relief for those who work on projects based on customers. Also, fewer individuals lead to fewer human errors that intimidate automated processes.

Compliance with privacy laws and handling investigations- internal and external- are the highest insurance companies’ standards. The need to keep current with ever-changing laws that prescribe how privacy should be protected increases the issue’s importance.

In this area, robotic process automation can also help a whole lot. Since the program produces comprehensive records of all transactions, it becomes much simpler to monitor the procedures and ensure that regulatory enforcement is in place. Therefore, external investigations are much less concern for insurance firms that use automation.

Blockchain

Since the advent of blockchain technology, we have seen the rise in its use and how it benefits various industries. The insurance sector can’t seem to avoid blockchain technology’s advantages. We have already seen a rise in the usage of blockchain development by major insurance industry players like AIG, Allianz, etc.

Integrating blockchain reduces administrative burdens and costs, improves security, and allows information sharing easily. Since the data stored on the blockchain is secure and cannot be altered, it can also help reduce insurance fraud.

Predictive Analysis

Predictive analysis is a branch of advanced analytics that helps predict future outcomes using historical data. Insurers use it to gain meaningful insights and understand customer behavior. Various insurance companies are using predictive analytics to find out the risk status, frauds, outlier claims and future trends, which helps them in avoiding any mishaps and losses. It is being used extensively and is expected to be used with more and more precision in the future.

Low Code

The rise of low-code development platforms has been in trend for a couple of years. It comes with various benefits, as applications developed using these platforms reduce the dependencies on developers and allow companies to develop and deploy updates much faster.

The insurance sector has also seen a rise in the use of these platforms, and the usage of these platforms is growing rapidly as they make managing apps easier. Low-code development platforms have taken over the market quickly. The insurance sector is also one of the markets adapting to these new platforms, as it has various benefits and can see massive growth in its usage over the coming years.

Chatbots

According to the research conducted by Finance Digest, more than 95% of all customer interactions will be powered by chatbots by 2025. Thanks to AI and machine learning, talking to customers through chatbots will become easier and more seamless.

The bots will be able to explain the policies and processes and answer customer queries without human intervention, saving the insurance companies a lot of time and cost. It also allows seamless interaction with the customers and 24×7 support. Some organizations are already using bots to interact with their customers, and this trend will continue to grow.

Personalization and Data

We live in an era where we are always connected with our devices, which constantly collect information about what we do, what we search for and what our interests are. Devices like smartphones and wearables collect the data and share it with organizations help them understand our needs and allowing these organizations to view customers as an individual rather than segment.

Insurance companies use this data to identify the needs and wants of their customers and create policies tailored to their needs. Using data to target customers allows for a better customer experience and also helps in accurate risk assessments.

Challenges for Insurtech

Evolving Competition

Competition is everywhere; no matter the industry, organizations try to find every opportunity to make their place and gain new customers. The insurance industry has also seen a massive rise in competition thanks to digital transformations.

These new trends have helped improve the customer experience and allowed new-age insurtech companies to play and dominate in the market. To keep up, the existing players need to improve their tactics and adapt to new technologies, which can be challenging for many organizations.

Maximizing Conversions and Improving Sales

Adopting digital transformation is not enough; maximizing conversions and converting your prospects to customers is the ultimate goal. Going digital can become overwhelming sometimes; companies might get thousands of visits on their websites or mobile apps but might not convert any of them into actual paying customers.

So, they have to focus on adopting digital transformation improving their customer experience and offering a personalized experience to increase their market potency.

Conclusion

The insurance industry is right to stick to its creative efforts and accept its market’s digital transformation. Now is the right time to seize all the opportunities for insurers to change their companies, how they work, and how they serve their customers.

This is the time for insurance companies to expand established partnerships and relationships to operate effectively and offer goods and services that comply with the customers’ expectations, drive progress and alleviate insurance companies’ pressure points. Insurers and insurtechs should reimagine what insurance can be and ensure that it meets the world’s needs.

These edge-cutting Insurance technology trends mentioned above bring in a fundamental transformation in the marketing and working of insurance companies. The insurance industry’s future is tailored policies, high connectivity, quick transactions, and constant information flow.

Frequently Asked Questions

IoT development is a tech solution for insurance. It can enhance customer experience and identify fraudulent claims.

AI can automate the entire insurance process, handling everything from applications to claim settlements without human involvement.

The incorporation of technology in the insurance sector is enhancing efficiency, transparency, and, above all, adopting a more customer-centric approach.